[Front page] [Contents] [Previous] [Next] |

Economic Instruments in Environmental Protection in Denmark

10. Implementation of economic instruments in Denmark

10. Implementation

of economic instruments in Denmark

10.1. Introduction

10.2. The concept of implementation

10.3. Implementation of

Environmental Taxes

10.3.1. Announcement

10.3.2. Supervision

10.3.3. Calculation

10.3.4. Collection

10.3.5. Control

10.3.6. Sanctions

10.3.7. Monitoring

10.4. The implementation of user fees

10.5. The

implementation of user fees versus taxes and charges

10.6. Main actors in the

implementation process

10.7. Conditions

for an effective implementation of economic instruments

10.7.1. Morality and acceptability

10.7.2. Efficient

collection and control mechanisms

10.7.3. Co-ordination at ministry

level

10.7.4. Simple

designs facilitate easy implementation

10.7.5. Comprehensive

environmental tax laws

10.7.6. Standardisation of tax laws

10.7.7. Economic

instruments are not vulnerable to implementation distortions

10.7.8. Conclusion

10. Implementation of economic instruments in Denmark

10.1. Introduction

Purpose of chapter

This chapter[1] describes the processes involved in the Danish implementation of economic instruments in environmental protection. Based on the Danish experience it seeks to identify factors of general importance to an effective implementation process.

The chapter is centred on six important aspects of the implementation process: announcement; supervision; calculation; collection; control; and sanctions.

Major issues

Some of the major issues addressed in this chapter are:

| the actors involved with the implementation process, and the division of tasks between them; | |

| the principles underlying the implementation policy, for example, in regard to the design of environmental taxes; and | |

| factors of importance to achieving a cost-efficient implementation. This includes also a discussion on administration and management issues. |

Delimitation

The chapter focuses on taxes and user fees.

10.2. The concept of implementation

Implementation and the decision-making process

Implementation is the process where a policy decision is put into specific action. It constitutes an important stage in the decision-making process, as it provides the link between the wishes and intentions of the political decision-makers on one hand, and the affected agents on the other (be it households or industrial sectors). Civil servants provide the realisation of this link.

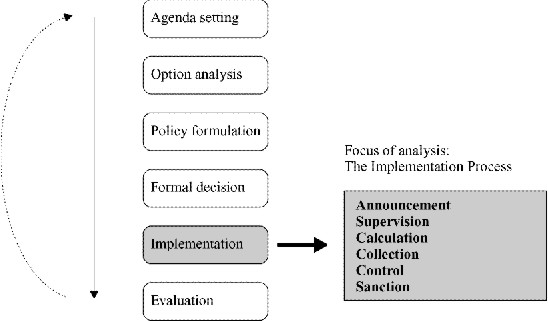

Figure 10.1 is a simplified illustration of a decision-making process. It should be noted that enforcement issues, such as control and sanctioning, are included here.

Figure 10.1

Stages in the policy process

The ideal implementation process

Ideally, the implementation process should lead to goal fulfilment at the lowest costs. However, the achievement of this ideal is a complicated task. Complexities arise for a number of reasons

| First, the above ideal outcome assumes, for instance, that all the affected economic agents can be identified, that they are all aware of the new regulation, and that they are being properly guided by the authorities on how to cope smoothly with the regulation in question. | |

| Furthermore, the tax level must be efficiently calculated, collected, and administrated. There should also be an effective control of payments compliance within the provisions of the law. If this is not the case, appropriate options for sanctions should be identified and used. |

All of these aspects will be examined in the following analysis of the six aspects of the implementation process shown at the right side of Figure 10.1.

10.3. Implementation of Environmental Taxes

10.3.1. Announcement

The announcement of new legislation aims simply to make citizens and enterprises aware of its existence. Legally, it is sufficient that an Act or Statutory Order is published in the Danish legal gazette “Lovtidende”.

Every citizen in Denmark is thereafter bound to comply with the regulation. However, it is generally recognised that the legal gazette is not the most appropriate means of ensuring that all relevant parties and persons actually become familiar with the law in question. As a consequence, the real channels of communication are very important.

These real channels of communication – the concrete supplementary means of announcement – have a number of variants. Variants include, for example, direct letters to affected enterprises, advertisement campaigns in major newspapers, television spots, and involvement in the announcement phase of the relevant industry or interest organisations.

Taxes are to be announced by the Danish Ministry of Taxation. It is the Department of Customs and Excise that exercise this duty. The Department is thus responsible for the preparation of information on new legislation. The means of announcement differs according to the specific context of the legislation. Text box 10.1 provides specific examples.

Text box 10.1 Examples of means of announcement

Announcement of the tax on pesticides The tax on pesticides entered into force on January 1, 1996. Technically speaking, the law contains a relationship between the importers and producers of pesticides (the parties imposed with the tax) and the taxation authorities (the collectors of the tax). The ultimate intention of the tax is to provide the users of pesticides, in particular the Danish farmers, with an economic incentive to reduce their use. The communication (announcement), however mainly targeted the producers and importers that have been guided on how to cope with the new regulation, and not the farmers. A major rationale for this, is that the farmers are the ones to react according to the new price structure. The information did not aim to pursue an awareness-oriented objective, but rather to inform those to whom the tax was imposed on, and how to deal with it. Announcement of the tax on tap water The announcement of the recently introduced tax on tap water exhibits similar features. Ultimately, the tax affects the whole Danish population. Technically, however, it only relates to the water utilities. The tax is collected from the water utilities (water works), who may, and do, pass it on to consumers. Still, it should be noted that awareness building measures have been used, in terms of, for example, public information campaigns, to encourage consumers to reduce their use of tap water. This has also included information on the economic gains to be achieved. These two examples show that the announcement activities do not, per se, have a broader “awareness-building” function, but primarily a legal purpose: to inform those which the law explicitly addresses. |

The Ministry of Taxation emphasises that enterprises affected by a new regulation should be informed properly and in due time. Experience shows, however, that this can be difficult. One important explanation of this relates to timing, particularly in cases where the adoption of a new tax or charge has constituted part of the approval of next years state budget. The budget is typically approved in December, and consequently, the new tax or charge takes effect already from January 1, the following year. This tight schedule does not leave much room for a well-prepared strategy of announcement, hence this process has given rise to severe criticism.

10.3.2. Supervision

The term “supervision” covers all activities that authorities undertake to guide the enterprises (and others) on how to comply with specific regulations, including economic instruments. Supervision basically aims to achieve the highest possible level of compliance at the lowest costs. This is to be achieved by providing the enterprises with as much relevant information and guidance as possible.

The Ministry of Taxation must elaborate specific guidelines on each new tax. If possible, the relevant industry organisations will often be involved in this process. The advantage of this involvement, is that the organisations know more on how to best communicate with their members regarding their specific conditions. Often, the involvement of industry organisations will enhance the relevance of the guidelines, and contribute to ensure a good communication of them.

The regional customs and excise departments play an important role in the supervision phase. They provide day-to-day supervision to the enterprises. This includes activities such as: the organisation of general information meetings; meetings with individual enterprises; organisation of seminars with specifically targeted enterprises; meetings with branch organisations; visits at enterprises; and the answering of phone calls and letters. provides an example of the announcement and supervision activities related to the CO2 tax in Denmark.

The philosophy underlying the supervisory activities is contained in the Strategy Paper of the Department of Customs and Excise (1998). The Department aims to achieve an active dialogue with enterprises and citizens. The dialogue should facilitate the dissemination of information on how to comply with the tax. Further, the dialogue would contribute to frame decisions that are “fair, coherent, and understandable”, while also giving a high priority to a strict policy that aims to ensure a high level of compliance.

Text box 10.2 The introduction of CO2 tax in Denmark

Shortly after the so-called CO2-package was introduced in 1995, advertisements were inserted in the major newspapers, followed by information campaigns published on the national television channels. In addition:

According to the Department of Customs and Excise, the above activities increase the level of compliance significantly. |

10.3.3. Calculation

The calculation of the liable taxes is the next step in the implementation process. It is a profound feature in Denmark, that this calculation is the responsibility of the enterprises liable to the tax. This system of “self-reporting” is applied at all levels.

The system of self-reporting implies that the tax is imposed on the highest possible levels of the distribution chain. This would typically imply that the tax is imposed on the producers and/or the importers of the article in question. In that case, all enterprises that produce and/or import the relevant article must register with the Department of Customs and Excise. All registered enterprises receive a certificate in proof of their registration.

On a regular, typically monthly, basis, the registered enterprises must assess and book the amounts of the dutiable articles that have left the enterprise and/or that it has used itself. The enterprises are obliged to report and pay accordingly.

The accounts resulting from the above thus constitute the basis for the calculation of the liable tax. Such a system requires both a good system of control, and a certain level of moral at the enterprises.

10.3.4. Collection

The 30 regional customs and excise departments collect the taxes. The regional departments are part of the Department of Customs and Excise. The departments have substantial experience and expertise that has developed through many years of practice with the collection of product taxes in Denmark.

The environmental taxes are thus collected by a “non-environmental” authority. The Department of Customs and Excise was not established to collect environmental taxes, however, the environmental taxation system in Denmark has been developed to make the most use of the already existing taxation system. The implementation of environmental taxes has thus been a major concern. In this regard, the use of an existing and well-functioning structure has considerably contributed to reduce the administrative costs involved in the implementation of the environmental taxes.

As a consequence of the above, the collection of the environmental taxes is quite efficient. The system of VAT registration is an important explanation for this. All enterprises in Denmark must register for VAT, and the VAT register in turn, constitutes the basis for the collection of VAT payments. This system is very effective, and it therefore provides an excellent basis for the collection of other taxes, including the environmental taxes. Through the register, the Department of Customs and Excise has a comprehensive and up-to-date register of all enterprises that undertake commercial activities in Denmark.

There are no statistics on the collection rates for environmental taxes. The Ministry of Taxation, however, assesses that the collection rates in almost all cases are at least 80%, and in the majority of cases, the rates are far in excess of 80%.

10.3.5. Control

The collection rates are strongly dependent on the effectiveness of the control system. While moral and willingness to comply are fairly high, control is nevertheless extremely important, to avoid evasion and misreporting.

Control of payment of environmental taxes is based on two pillars:

| all enterprises that produce and/or import dutiable products must register with the national Department of Customs and Excise; and | |

| enterprises are obligated to keep records of all transactions in the dutiable products. |

Comparisons of the records of relevant transactions (item 2 above) with the enterprise’s VAT reports facilitates a cross-checking of the accounts. Through cross-checking, mis-reporting and intended non-payments can be detected. Further, the system makes it possible for the taxation authorities to trace activities back in time. The Department of Customs and Excise can take action, such as inspection visits without prior notification. This option further contributes to render the system efficient, and such inspection visits do take place.

Text box 10.3 Examples of collection and control of taxes

The waste tax is imposed on the waste companies. There are less than 50 registered waste companies and this small number renders the task of collection and control relatively easy for the Customs Authorities. The companies must register with the Department of Customs and Excise, and they must, on a regular basis, prepare accounts on incoming and outgoing quantities of waste. The waste companies pass the tax on to the waste producers; simply by adding the tax on to the price that they charge to receive the waste. The CO2 tax is an example of a much more complicated system. The system applies a division of the energy consumption into three categories: heavy processes, light processes, and space heating. The taxes vary according to type of energy used. This implies that every single enterprise – not only the importers/producers of fossil fuels – must monitor the composition of its energy use and to pay the tax accordingly. |

Control is the responsibility of the Department of Customs and Excise and its 30 regional offices. The Department and the regional departments employ a total of 5,900 people. About one fourth of those are involved in various control functions. Correspondingly, about one fourth of the operation expenses are allocated to control purposes (estimated costs: DKK 700 million). However, no attempts have been made to assess the amount of resources used specifically for the control of compliance with environmental taxes.

Although significant resources are used for control purposes, it should still be stressed that the Danish tax system relies heavily on the existence of good moral and a willingness to co-operate with public authorities. As a rule, the taxation authorities estimate that 95% of all the enterprises can, a priori, be expected to comply with environmental taxes. This leaves the bulk of the control resources to be concentrated to a relatively small number of enterprises.

10.3.6. Sanctions

In principle, everyone can report a breach of law to the responsible authority and/or to the police. In the case of environmental taxes, it is normally the taxation authorities that report the offence. The possible financial sanctions relate to cases of delayed and omitted payments, and the provision of false information on the use of dutiable products.

The environmental tax laws contain slightly different stipulations on the types of sanctions to be applied. Hence, not all of the options for sanctions listed in the following may be applied in all cases. The gross list of possible sanctions include:

| cases of delayed payments, where the enterprise has to pay additional interests of the tax (1.3% per month); | |

| the imposition of fines; | |

| imprisonment of up to two years; and | |

| in severe cases, the Department may withdraw the registration of the enterprise in question until payment of liable amounts, including fines, has been effectuated. |

10.3.7. Monitoring

Another element of the implementation process is measuring the effects of the environmental taxes and charges. In Denmark, the monitoring of the environmental effects of environmental taxes and charges is not systematic. The environmental monitoring focuses on the quality of the environmental media; like air, soil, and water, and it does not aim to relate this in detail to the various instruments and regulations in use. The monitoring of environmental taxes and charges tend to focus more on the immediate behavioural effects achieved, and is still executed on a fairly ad-hoc basis.

The monitoring of the environmental effects on media affected by user fees, involves the municipalities, the counties, and the government. In the field of waste, the municipalities must report to the Danish Environmental Protection Agency on waste treatment. This makes it possible to monitor the fulfilment of overall national waste policy objectives. Tap water is monitored exclusively by the municipalities.

The counties are strongly involved in the monitoring of the aquatic environment by preparing the local recipient plans in accordance with the overall National Action Plan for the Aquatic Environment. The municipalities prepare sewage plans that must be in line with the local recipient plans. The common practice is to prepare the two types of plans simultaneously. If the counties tighten the quality requirements to the watercourses and lakes, the municipalities may need to improve the treatment facilities.

The use of environmental taxes is increasing, but the knowledge on the actual effect of the instruments is still rather limited. Therefore, ex-post evaluations are increasingly being carried out. Thus, evaluations were prepared in 1998 of the CO2 tax, the SO2 tax, the tax on chlorinated solvents, the sewage tax, and the tax on NiCd batteries[2].

10.4. The implementation of user fees

Announcement

User fees typically assume a relation between a municipality on the one hand, and its citizens and enterprises on the other. Comprehensive registers over households and enterprises are used. These registers constitute the prime source when identifying those affected by specific user fees.

The number of user fees is relatively small and stable. Consequently, the announcement of new fees is not a major concern. When a municipality or a group of municipalities, would launch a specific campaign to inform on, for example, changes in fee levels, this would typically be done in a fairly direct way: through the local media and/or through direct mail to all households.

Supervision

Each year, all households (owners of property only), and all other users of the relevant municipal service, are informed on the their use of the service and the associated liable fee payment. The municipalities are obligated by law to provide this information. Municipalities may also take other actions, such as the launching of specific information campaigns that could be targeted at specific groups.

The main supervision efforts are effectuated vis-ŕ-vis the enterprises. For example, some of the larger municipalities have employed a waste consultant. The waste consultant serves the enterprises, and provides advice on cost-saving measures to minimise waste production.

Text box 10.4 The use of local waste consultants.

| An inter-municipal waste company located in the southern part of Jutland, “Affaldsregion Nord”, has employed a waste consultant. The company is owned by six municipalities. There is a total of 800 enterprises in the region. The waste consultant visits the enterprises on a regular basis and provides advice on how to collect and sort their waste (in particular paper, plastic, & glass) more efficiently. So far it has resulted in a 5% increase in 1997 in the total amount of waste collected for reuse. The fact that such waste is not subject to the waste tax means that the enterprises have a potential financial benefit from the use of the advice. According to the waste consultant, there are many cases where the enterprises are not aware of the actual level of fees and taxes, and where they lack knowledge on cost-effective possibilities to reorganise their waste handling. The services of the waste consultant are offered to the enterprises free of charge. It is financed from the revenues from waste user fees. |

The Municipal Departments for Technical and Environmental Issues undertake the daily administration of the user fees. In undertaking this task, the departments co-operate with the Economic Department of the municipality[3]. Furthermore, the exact calculation of the user fees is done centrally by the company “Kommune Data” in Copenhagen. See Text box 10.5.

The municipal authorities calculate the fees for households. In the case of user fees that are determined by the actual use, the households and the enterprises are obliged to read their meters and report on their use. Meters are installed in most households and enterprises. If the reporting is omitted, the use is estimated. When a property is sold, an external party reads the meters. This mechanism ensures that the final payments will be correct in the end.

Some of the user fees are not quantity dependent. The municipal waste fee is normally set as a unitary price per household. User fees for industrial waste are calculated by the waste companies that receive the waste – they simply weigh in all the received waste.

Text box 10.5 User fees are calculated in a central computer system

| Calculation of the user fees is carried out centrally by the company Kommune Data, which is operated by the municipalities. It applies a specific computer program called FAS (Forbrugsafgiftssystem). The municipalities submit the necessary data to this company, the resulting fees are calculated, and the results are submitted to the municipalities. In some cases, KommuneData puts the results directly onto the property taxation documents. These documents are commonly applied to collect user fees. |

Collection

In practice, the collection of user fees from households is done simultaneously with the collection of property taxes. This facilitates a simple and effective procedure in case of delayed or omitted payments.

The collection of user fees from enterprises differs, to some extent, from the above. These fees are, in some cases, paid directly to the utility that provided the service. The utility is very often owned by the municipality or by in inter-municipal ownership.

Control

Control is performed by the municipal authorities when payments are not effectuated directly to the relevant utilities. The existence of comprehensive and up-to-date registers substantially contributes to provide the basis for an effective control. Further, the fees are designed so that evasion is difficult (see chapter 7).

Sanction in case of non-compliance

In the case of delayed or omitted payments, sanctions are imposed. This includes, for example, the imposition of interests and surcharges. Further, incorrect or omitted payments may lead to the following sanctions:

| dunning letters (reminders) with a fixed additional payment; | |

| collection of debt and/or debt recovery (inkasso); and | |

| mortgage may be taken out in real property. |

It should be noted that a municipality is not allowed to interrupt the provision of the service. However, the fact that the municipality may take out a mortgage in real property without a prior decree, substantially contributes to ensuring that payments are ultimately effectuated.

10.5. The implementation of user fees versus taxes and charges

There are important differences between the implementation of user fees and the implementation of environmental taxes and charges. This section identifies and categorises these differences.

Legal basis deviate

One should note that the legal basis for user fees and for environmental taxation is different.

User fees are implemented in a decentralised manner, whereas the implementation of environmental taxes is the responsibility of national authorities (the Ministry of Taxation and its subordinated authorities).

The municipalities set the user fees within the framework established in national legislation. This decentralised approach implies that local features, such as the state of the aquatic environment, may be taken into account. It further means that specific local priorities may be established and promoted within the frames provided by the legislation.

The Constitution states that environmental taxes and charges should be implemented by law. Consequently, there are several environmental tax laws in Denmark; one for each tax and charge. They are fairly standardised with regard to their structure and much of their content. This high level of standardisation does, in fact, provide the basis for a fairly standardised implementation process.

Table 10.1

The implementation of user fees, taxes and charges

User fees |

Taxes and charges |

|

Legal basis |

The Environmental Protection Act contains the mandatory requirements that must be made operational through local decisions. |

The Constitution and specific laws. Under the provision of the Danish constitution (article 34), taxes can only be collected if they are warranted by law. |

Principles steering the setting of rates |

Economic neutrality and full cost recovery (no more and no less) |

Guided by the overall aim to internalise external costs and/or set rates in correspondence with predetermined policy targets |

May the rates vary? |

Yes. Rates are fixed locally and separately. Rates may vary according to local conditions. |

No. Exceptions and tax differentiations may, however, be granted by law. |

Is the revenue ear marked? |

Yes. |

No. |

Prime implementing actors |

The 275 Danish municipalities. |

The Ministry of Taxation, Department of Customs and Excise (and its regional offices). |

Different principles for setting the levels

The principles governing the setting of fees and taxes are not the same. In principle, environmental taxes should aim to internalise the external costs. However, in most cases, a more pragmatic approach is applied. This approach implies that the tax is set at a level that is expected to lead to the fulfilment of certain policy objectives that comprise a wider range of objectives, than those that are purely environmentally motivated. User fees, on the contrary, are to be set on the basis of the principle of cost-recovery.

Size of user fees may differ between municipalities

As a consequence of the principle of full cost-recovery the user fee levels deviate significantly from one municipality to the other. This reflects substantial variations in local conditions.

Different actors involved

Different actors are involved in the implementation of the two types of instruments. The implementation of taxes is, by and large, the responsibility of the Ministry of Taxation and its subordinated authorities. The implementation of user fees is primarily the responsibility of municipalities. The municipalities are also overall responsible for the provision of the service in question. They might out-source some of the activities to private companies, for example, municipal waste collection, but they would still have to administer the overall arrangement, and would still assume overall responsibility.

Table 10.2

Actors involved in the implementation process

Implementation aspects |

Actors involved | |

Announcement |

User fees Taxes |

The municipalities |

Supervision |

User fees Taxes |

The municipalities |

Calculation |

User fees Taxes |

The municipalities (citizens and enterprises) |

Collection |

User fees Taxes |

The municipalities |

Control |

User fees Taxes |

The municipalities |

Sanction |

User fees Taxes |

The municipalities |

10.6. Main actors in the implementation process

This section describes the main actors involved in the implementation of environmental taxes.

Ministry of Taxation

The Ministry of Taxation is involved in three overall tasks:

| Framing of legislation; | |

| Administration of complaints from citizens and enterprises; and | |

| General administration and implementation of tax issues in Denmark. |

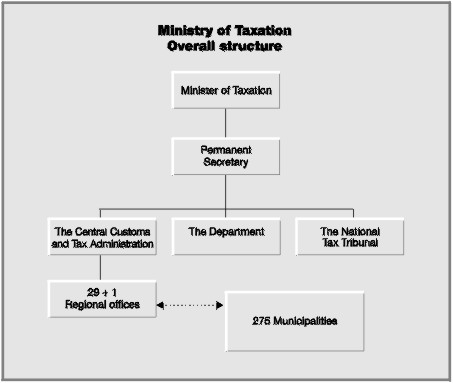

Figure 10.2

shows the organisation of the Ministry of Taxation

Consequently, the Ministry of Taxation is an important policy-maker in regard to economic instruments. The Ministry is formally responsible for the initiation and preparation of new environmental taxes. Normally, the Ministry will effectuate this in close co-ordination with the Ministry of Environment and Energy and other relevant ministries (for example, the Ministry of Foreign Affairs, the Ministry of Transport, the Ministry of Finance, and the Ministry of Trade and Industry).

Three specific offices in the Ministry are primarily responsible for the framing of new legislation on environmental taxes. In total, about 15 Ministry employees are, to some extent, involved in issues that relate to environmental taxes.

The Department of Custom and Excise

The Department of Customs and Excise is in the Ministry of Taxation. The department is responsible for the administration of taxes, charges, and customs in Denmark. The Department is a unitary organisation, but has delegated powers to 31 regional Custom and Excise Departments. The regional Departments carry out most of the implementation functions. The national Department announces new environmental taxes to the public and to the enterprises, and also regularly guides the regional Departments.

The Customs and Excise Regions

The Customs and Excise Regional Departments handle all issues in their specific regional area. This covers: the registration of enterprises; the handling of controversies over the interpretation of laws; reporting on VAT and other various types of taxes; and social security contributions. Furthermore, the regional Departments: answer inquiries from enterprises; produce information materials; organise courses for local enterprises; and visit enterprises. The regional departments also play a prominent role in the daily administration of environmental taxes and charges. They are thus responsible for the enforcement of the green tax laws. This responsibility includes: the supervision of enterprises; the collection of revenues; and the control of payments.

The Department of Customs and Excise employs a total of 5,900 people.

The Ministry of Environment and Energy

The Ministry of Environment and Energy is in charge of administrative and research tasks in the area of environmental protection, energy, and planning. Further, the Ministry plays a prominent role in the overall environmental policy making process. At regional and local levels, much of the administrative responsibility has been delegated to local governments in counties and municipalities. The Ministry employs more than 3,000 people. Figure 2.2 shows the organisation of the Ministry.

The Ministry has three agencies: The Danish Environmental Protection Agency; The Danish Energy Agency; and the National Forest and Nature Agency. The former is in charge of environmental issues. This includes also the economic instruments in environmental protection.

The Danish Environmental Protection Agency

The Danish Environmental Protection Agency (DEPA) has some 460 employees. The Danish EPA advises the Minister for Environment and Energy and administers legislation on the environment. The aim is to prevent and combat pollution of the water, soil, and air. The Danish EPA is organised into 24 specialist divisions, six interdisciplinary divisions, and the management.

The Economy Department in DEPA is responsible for environmental economic issues, including co-ordination of the Agency’s work in this field. Given the positive attention which is paid to the virtues of economic instruments in environmental protection, it comes natural that DEPA is a driving force in policy-development in this area, although the formal right and responsibility to prepare new legislation lies with the Ministry of Taxation.

The Energy Agency

The Danish Energy Agency was established in 1976. The Agency centres its activities around the production, supply, and consumption of energy. The Agency is responsible to ensure, on behalf on the State, a sound development of the energy sector in Denmark from the perspectives of society, the environment, and the security of supply. The Agency drafts and administers Danish energy legislation.

The Agency became involved in the implementation of economic instruments when the so-called CO2-package was launched in mid 1990s. The Energy Agency is assigned the right to enter into voluntary energy agreements with enterprises.

10.7. Conditions for an effective implementation of economic instruments

The appropriate methods to ensure an effective implementation of economic instruments in environmental protection are largely dependent on the specific conditions of the country in question. Such features and conditions may vary substantially throughout the world. This section identifies and describes seven factors that have contributed significantly to an effective implementation of economic instruments in Denmark.

10.7.1. Morality and acceptability

The first factor is of a very general and intangible nature. This factor relates to the existence of a certain morality in Denmark which renders it natural for the majority of enterprises and citizens to comply with existing legislation. Thus, it is the overall perception that most of the enterprises can be expected, a priori, to co-operate and comply.

Authorities are considered legitimate

This moral feature has evolved over time and its creation and persistence may, among other things, be explained by the fact the Danish authorities are generally perceived to be legitimate and competent authorities that do not misuse their power vis-ŕ-vis the citizen and enterprises.

Another important driving force behind the development of a certain morality, could also be the fact that a co-operative approach is often applied in the framing of policies. The approach implies that affected parties and other stakeholders are consulted while the law is prepared. This process is not a negotiation, but it can nevertheless contribute to the ensurance that unintended and unpopular side-effects are reduced. The law is also designed with a view to easing the administrative burdens of those imposed with the tax. Furthermore, the process implies that stakeholders might become more aware of the environmental issues dealt with. Consequently, the process can contribute to enhance the acceptability of the resulting legislation.

10.7.2. Efficient collection and control mechanisms

Registration systems

Effective collection and control systems are other very important conditions to an effective implementation of economic instruments. The collection and control systems in Denmark make it difficult to evade tax payments. Effective registration systems is an important aspect of this:

| A national register (“Folkeregistret”) stores information on all Danish citizens (for example, the date of birth, place of residence, and profession). In order to be entitled to social services, and other public services, citizens must be registered. Hence, there is a very strong incentive to register. All citizens are registered at birth. | |

| Households are registered on a municipal basis and this registration forms the basis for payment of property taxes and other services. The authorities thus have complete information on all households. | |

| All enterprises must register with the VAT register. |

10.7.3. Co-ordination at ministry level

Co-ordination is a necessity

The effective use of economic instruments necessitates a strong co-ordination of communication between the Ministry of Environment and Energy on the one hand, and the Ministry of Taxation on the other. This applies to the preparation stages, as well as to the implementation process.

Co-operation has been substantially enhanced since 1993. Until 1993, the Ministry of Environment and Energy was quite isolated in its intention to enlarge the use of economic instruments. The Ministry of Taxation was somewhat reluctant, with the exception of energy taxes and taxes on vehicles.

Since 1993, however, three major policy initiatives and studies have contributed to place the merits of environmental taxes higher on the political and administrative agenda. The initiatives and studies include: The 1994 tax reform; the so-called Dithmar-analysis, which studies the options for a wider use of environmental taxes in Denmark; and the action plan for the aquatic environment (“Vandmiljřplan II”). These studies span across the bureaucratic borders of the ministries, and have resulted in a spread of understanding and support of the basic rationale behind environmental taxes. The establishment of forums for debates, and consultations with representatives from environmental, economic, and taxation authorities, have all been of significant importance to this process.

Formal initiative right rests with the Ministry of Taxation

The Ministry of Taxation has the formal right to prepare and forward environmental tax laws. Thus, the recent changes of the Pesticide tax (1998) was prepared almost solely by the Ministry of Taxation. The Ministry of Environment and Energy was involved only to a minor extent. This illustrates that the Ministry of Taxation has moved from a position of reluctance towards a position where it actively promotes environmental taxation.

10.7.4. Simple designs facilitate easy implementation

The administrative costs

Effective implementation can be seriously be impeded by an inappropriate tax design. It is therefore important to assess the administrative, monitoring, and compliance costs of the implementation of specific user fees and taxes. Issues to consider relate to, among other things, the choice of the tax/fee base (object for taxation). The base should be easily identifiable, calculable, and controllable. This identification of the base will often necessitate trade-offs and the acceptance of a compromise between the ideal environmental performance, and the need to use a cost-effective means of administering the tax. Over the years, simple designs have come to play a prominent role.

The Danish tax on ozone depleting substances (ODS) provides an example of such a simple design. The tax is DKK 30/kg for all types of ODSs and halons, even though the ozone depleting potentials of these substances vary significantly (with more than a factor 10 between the most and the least depleting substance). There is thus only a weak correlation between the relative environmental undesirability of the substance and the tax level. Hence, the environmental precision can be said to be low. The unitary tax level, however, eases the implementation of the tax.

As a rule of thumb, it is generally required that the administrative costs of a specific environmental tax must not exceed 5% of their total revenue. If the percentage is higher, the administrative costs are considered to be unacceptable.

For the same reason, Denmark prefers product taxes to emission taxes, although the latter are more closely related to the environmental problems. In fact, genuine emission taxes are not used at all in Denmark, because control and measurement is difficult and costly. Still, the sewage tax and the SO2 tax bear a strong resemblance to emission taxes.

10.7.5. Comprehensive environmental tax laws

Ideally, an environmental tax law should identify the problem(s) to be addressed and stipulate the objective(s) to be pursued. Furthermore, it should structure the implementation process. The latter means that the law should, for example, specify the authorities responsible for the specific implementation functions, provide the legal and financial resources to those authorities, stipulate a set of clear and consistent objectives, and assign implementation functions to the relevant agencies that support the legislation’s objectives.

In general, the laws on environmental taxes in Denmark fulfil these criteria quite well. Thus, as one of the first clauses, all environmental tax laws would contain a statement where the problems to be addressed and the objectives of the new law are explicitly mentioned. Further, all the laws contain an explicit identification of the responsible taxation authorities responsible. Finally, an assessment of the administrative costs normally accompanies the laws.

10.7.6. Standardisation of tax laws

The Danish tax laws are, to a high degree, standardised. They follow the same outline, stick to same principles regarding tax design, and the taxes are typically product taxes.

Table 10.3

Composition of the Danish environmental tax laws

The tax is imposed high up in the distribution chain; meaning at the level of the producer and/or the importer of the product (goods, substance, etc.), who is to be taxed. One notable exemption from this “standard” is the CO2 tax law, where refunds are provided to the individual companies. |

All enterprises that produce and/or import the relevant product must register at the national Department of Customs and Excise as producer/importer of the product in question. All registered enterprises receive a receipt. |

On a regular (monthly) basis, the registered enterprises must calculate and book the amounts of the dutiable products which have left the enterprise, and pay accordingly |

Dutiable products which are components in other non-dutiable imported products are taxed according to the specifications in the Danish Customs Law. |

Dutiable products which are exported are exempted from taxation |

Some uses of the product are exempted from taxation, for example, products used for diplomatic purposes |

If the tax is not paid at the latest of 14 days after it is due, the Department of Customs and Excise may withdraw the registration of the enterprise; hence, it is not allowed to operate until taxes are paid. If the tax is not paid in due time the enterprise shall pay 1.3% interest rate per month. |

The Department of Customs and Excise has the right to inspect the enterprise and the accounts without prior notification |

10.7.7. Economic instruments are not vulnerable to implementation distortions

Finally, it should be highlighted that the use of economic instruments in environmental protection has an implementation advantage that is seldom recognised. This derives from the fact that economic instruments are not as vulnerable to implementation distortions as other instruments.

Implementation distortions arise when the implementation process is distorted. The results of distortions are that the final outcomes are not in accordance with the initial expectations. Such distortions may arise from the fact that implementation is more than a pure technical exercise. Implementation is often a political issue in which disputes over (re)distribution of societal resources can take place, resulting in a distortion.

Furthermore organisations and individuals are the actual executors of the implementation. They may also intentionally or unintentionally bias the final outcome compared to the political intentions.

Economic instruments leave very little room for such policy making at the implementation stage. Once the law is completed, it is only the small details that are left for the interpretation of the Minister and the administration.

Another implication of the above is that unresolved disputes can only very rarely be transferred to the implementation stage in the case of economic instruments.

10.7.8. Conclusion

Table 10.4 provides an overview of the previously identified factors of importance to the effectiveness of the implementation process.

Table 10.4

Overview of factors of importance for effective implementation of economic instruments

Factors of importance for implementation |

Consequence for the implementation process |

Other consequences |

Moral standards within the general public and the enterprises |

Makes it possible to have a system in which enterprises themselves, “self-report” on consumption of dutiable products. Moreover, the taxation authorities can concentrate its control efforts on 5% of all the enterprises, assuming the rest will comply voluntary. |

|

Effective collection & control systems |

Collection rates are quite high (estimated to more than 80%, and much higher in most cases). Difficult to evade. |

|

Co-operation between the Ministry of Taxation and the Ministry of Environment and Energy |

Makes it possible to let the taxation authorities be in charge of the implementation of environmental taxes, even though this is a relatively “new” task for tax authorities. |

The Ministry of Environment and Energy may influence the Ministry of Taxation, and other ministries, with “green” thinking. |

The taxes are designed simple and with a an emphasis on administrative feasibility |

Keep the administrative costs at a low level. Should not exceed more than 5% of total revenue. |

The tax base must be rigid. In some cases the tax will not reflect the environmental impact with a high precession. |

Comprehensive environmental tax laws |

Increases the likelihood that the laws will be implemented consistently and in accordance with the intention. |

|

Standardisation of environmental tax laws |

Makes it possible for the taxation authorities to build up routines in the implementation. |

Secure transparency |

Notes:

Important sources of information for this chapter are: interviews with representatives of the Ministry of Taxation, the Ministry of Environment and Energy, and the regional Customs and Excise Departments, together with Kommunernes Landsforening; “Environmental Administration in Denmark”, 1995, Ministry of Environment and Energy.

All these evaluations have constituted important sources of information for this report.

This description only concerns the relation between the municipality and the users it services. It does not consider the functioning of the system at the utilities actually providing the service, i.e. the sewage plant, the waste plant and the water works.

[Front page] [Contents] [Previous] [Next] [Top] |