[Front page] [Contents] [Previous] [Next] |

Economic Instruments in Environmental Protection in Denmark

5. Product taxes and charges

5. Product taxes and charges

5.1. Energy taxes

5.1.1. Purpose

5.1.2. Tax base

5.1.3. Collection and revenue

5.1.4. Assessment

5.2. Taxes on motor vehicles

5.2.1. Purpose

5.2.2. Tax base

5.2.3. Collection and revenue

5.2.4. Assessment

5.3. Tax on vehicle fuels

5.3.1. Purpose

5.3.2. Tax-base

5.3.3. Collection and revenue

5.3.4. Assessment

5.4. Tax on tap water

5.4.1. Purpose

5.4.2. Tax base

5.4.3. Collection and revenue

5.4.4. Assessment

5.5. Tax on certain retail containers

5.5.1. Purpose

5.5.2. Tax base

5.5.3. Collection and revenue

5.5.4. Assessment

5.6. Tax on disposable tableware

5.6.1. Purpose

5.6.2. Tax base

5.6.3. Collection and revenue

5.6.4. Assessment

5.7. CFC and halons tax

5.7.1. Purpose

5.7.2. Tax base

5.7.3. Collection and revenue

5.7.4. Assessment

5.8. Chlorinated solvents

5.8.1. Purpose

5.8.2. Tax base

5.8.3. Collection and revenue

5.8.4. Assessment

5.9. Pesticides

5.9.1. Purpose

5.9.2. Tax base

5.9.3. Collection and revenue

5.9.4. Assessment

5.10. Tax on growth promoters

5.10.1. Purpose

5.10.2. Tax base

5.10.3. Collection and revenue

5.10.4. Assessment

5.11. Tax on NiCd-batteries

5.11.1. Purpose

5.11.2. Tax base

5.11.3. Collection and revenue

5.11.4. Assessment

5. Product taxes and charges

5.1. Energy taxes

This section only describes the pure energy taxes. The CO2 tax and the SO2 tax are not covered by this description, as they are considered to be taxes on effluents rather than on products. Further, chapter 12 provides a thorough description of all economic instruments used in the energy sector, also including subsidies.

The Danish energy sector comprises a number of rather different sub-sectors. They differ, for example, with regard to market structure and organisation. Thus, the sector includes a fairly competitive oil market, as well as a centralised monopoly structure in the natural gas market.

The Danish electricity sector is divided into two independent areas, which are organised into regional associations responsible for overall power planning, load dispatching, and operation of their respective transmission nets. The total Danish primary energy consumption has remained fairly constant over the last decades. In 1997, it amounted to 837 PJ (20 million tons of oil equivalents), compared with 825 GJ in 1972.

The first energy taxes were introduced in 1977. They applied to oil products and electricity, and were mainly implemented as a response to the oil crisis of 1973. The taxes thus aimed to promote energy savings and to provide an incentive to substitute away from oil to other energy sources.

Energy production and use in Denmark comes from numerous sources. Of greatest importance are coal, oil, and since the oil crises in the 1970s, natural gas.

Total energy consumption has remained fairly constant during the last two decades. During the 1990s it has increased by only 0.3% p.a. However, the various primary energy sources’ share of the total energy supply has changed significantly. Denmark has gone from being almost totally dependent on imported oil, to the present situation with a diversified energy supply and a position as a net-exporter of oil. The current supply is based on oil (45%), coal (26%), natural gas (20%), and renewables (9%). Nuclear energy is not an option in Denmark according to a decision of the Folketing in 1985.

5.1.1. Purpose

The energy policy in Denmark aims to reduce the use of coal and to promote the use of natural gas, as well as renewable sources of energy, such as wind mills. This can be seen as a reflection of increased environmental awareness and a strong emphasis on the issue of self-sufficiency. These policy objectives have in the 1990s, been supported by changes in the energy taxes. Thus, levels of taxation for coal and electricity have increased. Additionally, energy taxes have generally increased during the 1990s.

Furthermore, the tax aims to raise revenue for the general budget. It also aims to reduce imports through lower private energy consumption.

5.1.2. Tax base

Energy taxes are levied on bottled gas, fuel oil, gas oil, coal, electricity and natural gas. The taxes are set, based on the energy content of the fuel in question. Energy taxes are input taxes, in the sense that they are levied on the fuels used for energy production. Electricity generation, however, constitutes an exception. Fuels used for electricity production are not liable to the tax. In this case, there is a tax on the output (electricity). Consequently, the tax in itself does not provide an incentive to shift to less polluting fuels in electricity production.

The motivation for taxing electricity rather than the fuels applied in electricity production should be found mainly in concerns over competitiveness. Electricity is traded across borders and it is not possible to track down the specific sources of energy that are used to produce one specific kWh-unit.

The tax rates have steadily been increasing. Total taxation (including VAT) amounts to about two thirds of the consumer price. The energy taxes mainly affect households. Most industries and other VAT-registered companies are exempted from energy taxes, with the exception of space heating. Since 1995, however, energy taxes have been levied on industrial energy consumption for space heating.

Table 11.2 illustrates the current and planned tax rates for the major energy sources.

5.1.3. Collection and revenue

The energy taxes provide large revenues as shown in Table 5.1. The main contributors are the taxes on oil and electricity. Electricity production is mainly based on coal. In 1997, 61% of the total fuel use in electricity production and CHP consisted of coal. Natural gas and oil accounted for 15% and 12% respectively. Renewable sources and other sources accounted for another 12%. The share of natural gas will increase significantly in the future; the result of an expected phase in of additional gas fired CHP plants.

Since the use of coal mainly takes place in the electricity production and by the industrial sector, it is largely exempt of tax. Similarly, natural gas only provides a minor share of the state revenue, as the major share of the “tax” on natural gas is collected as a shadow tax by the gas companies (this is further explained in chapter 11).

The energy taxes are levied on the oil companies that produce and import the fuels. Electricity taxes are levied on the power companies that produce and supply electricity. The Customs and Excise Department of the Danish Ministry of Taxation collects the taxes. Taxes are fully and explicitly passed on to consumers (including industry and other purchasers of heat and electricity).

In the case of industry, the energy taxes are largely refunded (with the exception of space heating) by the Customs and Excise Department, and are combined with the collection of VAT. When handing in VAT forms, the enterprises in question also specify (and prove) the energy taxes paid during the period in question. The energy taxes are deducted from the VAT, and only the net amount is paid.

Table 5.1

Revenues in 1998

Object for Taxation |

MDKK |

Oil Products |

6,241 |

Natural Gas |

122 |

Coal |

787 |

Electricity |

6,979 |

Total |

14,129 |

Source: Statsregnskab for finansĺret 1998

5.1.4. Assessment

The current structure of the energy taxes and their present levels present a compromise between various goals and considerations that are sometimes in conflict. The taxes have been designed to contribute to the achievement of certain environmental goals, while still recognising their significant fiscal contribution. Furthermore, concerns over income distribution and competitiveness have played a role in setting the taxes.

A major achievement of the Danish energy policy, in which the energy taxes play an important role, is that the traditional positive correlation between energy use and economic growth has been broken. In other words, economic growth is no longer accompanied by a corresponding increase in energy use.

As such, the energy taxes are relatively high in comparison with European standards. Their mere size thus provides an incentive for energy savings, particularly in households. The low level of realised taxes for the most heavy energy users may provide a limited incentive for energy savings in these sectors, whereas the potential benefits could be the largest in these sectors.

As mentioned above, all fuels used for electricity generation are exempt of energy and environmental taxes. Instead, the taxes are levied on the electricity. This design does not per se provide incentives for more efficient electricity production or for a switch to cleaner fuels. The taxes only give the end-user an incentive to reduce the consumption of electricity as such.

5.2. Taxes on motor vehicles

Denmark has one of the highest vehicle tax rates in the world. Taxes on vehicles were originally intended as a tax on luxury goods. Further, as Denmark does not have a car manufacturing industry, the vehicle tax system can also be considered as a means to control the balance-of-payments.

The taxes on motor vehicles are comprised of:

- A registration tax, which is a tax paid upon purchase of the vehicle (heavy trucks are excluded); and

- An annual tax based on the fuel economy of the vehicle. Liability to the tax occurs once the possession of a vehicle has been registered in Denmark, and all vehicle owners are liable to the annual tax. Known as ‘The Owners Green Tax’ in Denmark, the tax entered into force in 1997 and applies to all new vehicles. Before 1997, the annual tax was based on the weight of the car. All vehicles sold before 1997 are liable to the annual weight based tax.

5.2.1. Purpose

The main and original purpose of the registration tax and the annual vehicle tax is to raise revenue. Further, the vehicle taxes are motivated in a wish that vehicle owners should bear some of the costs involved in the construction and maintenance of road infrastructure. Today, the registration tax also explicitly aims to reduce the number of vehicles in Denmark, and to provide an incentive to use smaller vehicles with better fuel economy.

5.2.2. Tax base

All vehicles in Denmark are liable to the taxes. Registration is a condition where all cars must have licence plates. The registration tax is paid upon registration.

The presentation below includes a detailed description of the system that applies to passenger cars. As mentioned above, heavy duty trucks are excluded. Further exemptions and other variant schemes apply to light duty trucks and vans, and other specified vehicles such as taxis. Basically, these vehicles are taxed lower than the passenger cars.

However, it should be noted that the registration tax for vans was increased in 1994 in order to reduce the private use of vans, and to provide an incentive to buy smaller vans. For vans between 2 and 3 tons, the tax was increased from DKK 12,000 to DKK 30,000. For vans between 3 and 4 tons, there was an increase from DKK 7,500 to DKK 19,000.

The Danish registration tax is very high compared with other countries. It amounts to 105% of that part of the value of a new passenger car that is below DKK 50,800 (1999 level), and 180% for the rest. The basis for calculation includes 25% VAT, custom duties[1], and profits to the retailer. This means that the registration tax is also imposed on the VAT and on the retailer’s profit. To encourage the import and use of safer vehicles, vehicles equipped with air bags and with ABS systems are entitled to a deduction in the tax.

The taxation of motor vehicles tends to shift gradually from the registration tax to annual taxation as the most important one. This means that the fuel economy of the vehicles will increasingly influence the taxation level in the future.

Table 5.2 provides illustrative examples showing the composition of prices of vehicles sold in Denmark. The table provides examples of the ultimate consumer price of three passenger cars. Before taxes, the prices are assumed to be DKK 50,000, 80,000, and 100,000 respectively. These prices include profits to importers and retailers. The ultimate consumer prices, i.e. the prices including VAT and registration taxes, for these three examples, amount to DKK 124,795, 229,795 and 300,605 respectively. Thus, the total tax burden amounts to between 150% and 201% (for these three examples) of the import price, including the profit to the importer and the retailer.

The fact that the tax rate increases to 180% for the part of the tax base that exceeds DKK 50,800 provides for a progressive effect of the registration tax. Higher income groups may be assumed to buy more expensive vehicles, hence they will be imposed with a relatively higher registration tax. For example, the price difference (net of all taxes) between the cheapest and the most expensive car in table 5.2 is 100%, but the consumer price difference (including all taxes) becomes 140%.

On average, the annual tax according to weight amounts to about DKK 2,900 annually. For new cars, the annual tax is based on energy consumption, and (Owners Green Tax) is charged according to km/litre of a vehicle. Vehicles with good fuel economy are subject to a smaller tax. Thus, the large and more energy-intensive vehicles are taxed more heavily. Diesel-powered vehicles are taxed higher than petrol-driven vehicles, but the tax on diesel fuels is much less.

Table 5.2

Taxes imposed on a petrol powered passenger car (excludes profits to importers and

retailers – profits are also liable to the taxes)

Price component |

DKK |

DKK |

DKK |

Import price of vehicle with ABS and air-bags |

50,000 |

80,000 |

100,000 |

VAT, 25% |

12,500 |

20,000 |

25,000 |

Deduction for ABS and air-bags |

6,725 |

6,725 |

6,725 |

Tax base |

55,750 |

93,275 |

118,725 |

Registration tax |

|||

105% of 50,800 |

53,340 |

53,340 |

53,340 |

180% of (tax base -50,800) |

8,955 |

76,455 |

122,265 |

Total (Import price, VAT and registration tax) |

124,795 |

229,795 |

300,605 |

5.2.3. Collection and revenue

All vehicles in Denmark must be registered with Central Registration. This is stipulated in the Road Traffic Act. In 1996, the registration tax constituted 52% of the taxes on vehicles, and the annual weight-tax 17% (other taxes account for the rest).[2] The two taxes are collected by the Department of the Central-registration of Motor Vehicles. The Department is under the Ministry of Justice.

Registration tax: It is the Department of Customs and Excise that collects the tax from the vehicle retailers. In order to be registered as a dealer, a license must be obtained. The obligation to register and the register itself constitutes the core of the collection schemes for vehicle taxes. All new cars must be registered, and changes of ownership must be reported to the Central-registration of Motor Vehicles. The registration tax is only paid at the first registration of the car. After the first registration, the vehicle can be sold freely without any additional taxes. In 1998, the registration tax provided a revenue of MDKK 18,290 to the state budget. Due to an increase in the import of new cars, the registration tax has increased over the last years. About 83,000 new vehicles were registered in 1993, compared with 142,000 registrations in 1996. Thus, there has been an increase in the amounts collected. In 1993, it was MDKK 7,998, and in 1996, it was MDKK 15,367.

Annual vehicle tax: The person who is registered as the owner of the vehicle is the one who is liable to the annual tax. Hence, there is a clear incentive to report changes of ownership to the register. The tax is paid by the registered owner of the vehicle via the Central Registration to the Department of Customs and Excise. Owners of new cars are liable to the Owners Green Tax. This tax is estimated according to specific standards set up by the Ministry of Taxation; all new cars are categorised into this particular scheme, which is based on the fuel economy of the vehicle (km/litre). All cars that were first registered before 1997 are liable to the weight based tax. If the tax is not paid the registration will be cancelled. A vehicle cannot be re-registered unless the liable tax has been paid. In 1998, total collection provided a revenue of MDKK 5,444.

The taxes on vehicles provide the largest contribution to government revenue of all the environmental taxes and charges applied in Denmark as shown in Figure 4.1. However, compared to other EU-member states, the Danish taxation on heavy-duty vehicles (trucks) is at the mid-scale.[3]

5.2.4. Assessment

The vehicle taxes are predominantly motivated in fiscal concerns, and they generate substantial government revenues. The administrative set-up renders evasion extremely difficult, if not impossible. The number of cars per capita in Denmark is estimated at 338 per 1000 inhabitants[4]. This number lies in the lower end compared with the other EU countries (between 223 (Greece) and 568 (Italy))[5]. Consequently, and in the light of the high GDP/capita in Denmark, the registration tax is likely to have a mitigating effect on the development in the number of vehicles.

It may be argued that the high registration tax may reduce the incentive to replace old cars with new ones, as the registration tax has the effect of making new cars relatively more expensive. However, the better fuel economy of new vehicles and concerns on safety matters (further supported by the above exceptions for ABS systems and air bags), may imply a weakening of this effect.

Further, the design of the annual tax and the registration tax both provide an incentive to purchase vehicles with good fuel economy. The more expensive and the heavier the vehicle is, the higher is the tax. It is typically the heavy and expensive vehicles that have the poorest fuel economy. This effect has been further supported by the increased taxes and vehicle fuels that resulted from the 1994 tax reform.

The fuel economy in Danish vehicles is generally high compared to other European countries. This indicates that the system as such, does not provide a significant incentive for vehicle owners to keep their old cars.

Denmark agrees with a proposal presented by the European Commission. The strategy proposal aims to increase fuel economy up to 20 km/l for petrol cars, and 22 km/l for diesel cars. As a result of the high taxation of vehicles, Denmark is in a good position to pursue this objective.

The new ‘Owners Green Tax’ also has an environmental objective. Rough and preliminary estimations of the new Owners Green Tax show that it has had some effect in this regard.

Finally, it should be noted that it is the transport activities that cause the environmental effects, rather than the possession of vehicles as such. In this regard, the vehicle fuel taxes have an important role to play.

The high registration tax may be argued to have an income-distributional effect, because it renders it fairly expensive to acquire a vehicle. Assessing the relative economic burden that the tax imposes on various incomes groups, it is typically concluded that the registration tax and the taxes on vehicle fuels have a relatively higher impact on the higher income groups than on the low-income groups.

5.3. Tax on vehicle fuels[6]

Vehicle fuels have been taxed in Denmark since 1927. The legal foundation is the Government Order on Energy Taxes on Mineral Oil Products of 28 September, 1998. Border-trade concerns and concerns related to the Single European Market have limited the scope of action for the Danish government in this field. The taxes are considered as a part of the energy tax system.

5.3.1. Purpose

The prime objective of the tax is two-folded: to generate revenue and to control imports of fuels. However, over the last decade, environmental concerns have become steadily more integrated into the vehicle fuel tax scheme. By increasing the fuel price, the tax can be expected to reduce the demand for vehicle fuels and diesel with a consequent positive impact on the environment (reduced exhaustion, noise, and congestion).

Environmental concerns first entered the vehicle fuel tax scheme explicitly in 1986, where unleaded petrol became subject to a lower level of taxation than leaded petrol. The level of tax differentiation was changed a number of times. In the 1990s, the differential typically resulted in a consumer price difference of about 7%. Tax differentiation was thus used as an explicit means of attaining an environmental improvement (the phase-out of lead in petrol). Today, tax differentiation is used in favour of fuels supplied with the use of vapour recovery installations. In these cases, the difference is DKK 0.03/litre.

A tax differentiation in favour of petrol with low content of benzene entered into force January 1, 1998. This scheme involves a gradual increase in the differentiation according to the benzene content. There are five levels. The difference between the highest level (benzene content between 4% and 5%) and the lowest level (benzene content less than 1%) is DKK 0.08/litre. By year 2000, only petrol with benzene contents lower than 1% can be sold in Denmark.

The increase in motor fuel taxes during the period of 1994-1998 was motivated in the tax reform from 1994. The increases are thus to be seen as an integral part of the efforts to reduce the burden of taxation for labour, and in turn, increase environmental taxation, and the efforts to control the demand for vehicle fuels.

The tax on diesel fuel is smaller than the tax on petrol. Today, the tax is about DKK 1 less than the tax on petrol. From June 1, 1999, tax incentives have been introduced for diesel with a sulphur content below 50 pmm. It is estimated that all autodiesel sold in Denmark in the near future will meet this specification. Diesel fuels are also subject to a CO2 tax of DKK 0.27/litre.

5.3.2. Tax-base

The tax on vehicle fuels is calculated as a fixed amount per litre of the various types of fuel: petrol, diesel, LPG, and natural gas. Consumer fuel prices tend to be at levels comparable to those applied in Germany. This is due to border trade concerns. Petrol taxes were raised (and diesel taxes lowered) in 1990, and industry became liable to the tax on diesel fuel in 1991. As a consequence of the tax reform from 1994, vehicle fuel taxes have increased substantially in the period of 1994-1998. Tax increases have been in the order of 20%. These increases are thus in line with the environmental approach taken in the tax reform. The resulting levels still correspond to the levels that apply in Germany. Table 5.3 shows the tax rates that were applied in 1998. It should be noted that all fuel types, except petrol, are also subject to the CO2 tax. This tax is further described in section 6.1.

Table 5.3

Vehicle fuel tax. 1999[7]

Vehicle fuel type |

DKK/litre |

Gas and diesel fuel |

2.35 |

Petrol* (with a no-lead lubricating additive) |

4.42 |

Unleaded petrol* |

3.77 |

Petroleum |

2.35 |

LPG |

2.63 |

*For petrol, two other tax differentiation schemes are in effect. The first contains a differentiation depending on the benzene content of the fuel, and the latter reduces the tax if vapour recovery installations are in place. The maximum difference according to benzene content is 0.08 DKK/litre, and the reduction in the case of vapour recovery amounts to 0.03 DKK/litre.

Households and VAT-registered entities are liable to the vehicle fuel taxes, whereas public transport receives a 100% refund. This means that public transport does not de-facto pay vehicle fuel taxes.

5.3.3. Collection and revenue

It requires a certain amount of transport volume per year for a diesel-driven car to be more economical than a petrol-driven car, i.e. to take advantage of the lower tax on diesel. This is, because the diesel-driven cars are more expensive to purchase. Thus, due to the design of the vehicle tax system, households typically use petrol-driven cars, whereas diesel is the most commonly applied motor fuel for commercial vehicles. Consequently, and because households have the largest share of the vehicles in Denmark, households contribute the highest share of the revenue generated from vehicle fuel taxes.

The revenue from the vehicle fuel taxes enters into the overall government budget. In 1998, the revenue from the petrol tax was MDKK 8,834[8] and the diesel fuel tax approximately MDKK 3,800[9].

As with all other product taxes, the tax is collected by the importers and producers of vehicle fuels. Collection at this level simplifies the administrative burden of collection and control.

It is the consumer of the vehicle fuel who pays the tax. Thus, the tax is paid every time the vehicle is filled up. Importers of vehicle fuels and gas stations must register with the Department for Customs and Excise. The Department collects the taxes from the importers of vehicle fuels, based on reports on sales of fuels. The importers must give financial security for the payment of the tax.

Typically, the taxes constitute about two-thirds of the consumer price for petrol fuels in Denmark. For diesel fuels, the tax constitutes about 1/3 of the consumer price, including the VAT.

5.3.4. Assessment

The prime objective of the vehicle fuel taxes has, for decades, been fiscal rather than environmental. In a fiscal sense, the taxes generate substantial revenues to the government. In recent years, however, environmental concerns are increasingly being taken into consideration. This is reflected in the enhanced use of tax differentiation to pursue environmental objectives. Further, the tax level has been increased since 1994 as part of the 1994 tax reform. These increases were motivated in the wish to increase environmental taxation, and thereby to establish the fiscal room for the lowering of the taxation of labour.

The vehicle fuel taxes add to the selling price of fuels. To the consumer, however, the relevant price is the fuel price per kilometre rather than the price per litre of fuel. As mentioned in the previous section, the fuel economy of vehicles tend to be improved year by year, and this process may be further accelerated if a common EU effort is implemented, aiming at an ultimate 20% improvement.

Consequently, for the fuel taxes to actually provide an incentive to reduce the number of kilometres driven, they must be set with a view to both the current production price of fuel (which varies), and with a view to the developments in the fuel economy of vehicles.

The demand for fuels has been little affected by tax increases. This is most likely explained by an increase in the demand for transport, possibly resulting from the above improvements in fuel economy of new vehicles. Thus, it may not necessarily be a reflection of insensitivity of demand to fuel prices.

Evidence, however, suggests that tax differentiation schemes have an effect. This applies in particular to the role played by tax-differentiation in the phasing-out of lead in petrol.

In 1986, unleaded petrol had a market share in Denmark of almost nil. By 1994, leaded petrol was completely phased out in Denmark. The tax differential has been one of the driving forces behind this phaseout. The process was further supported by a number of other measures, which included: 1) a gradual lowering of the limits for the content of lead in leaded petrol, 2) emission limits (as from late 1990) necessitating the need for catalytic converters in new cars (which in turn need unleaded petrol to be effective), and 3) awareness building, in terms of, e.g. information campaigns to overcome consumers’ reluctance as to the applicability of unleaded petrol. The tax differential had a direct effect in terms of directly affecting consumers’ demand. Further, it had an indirect effect through its impact on the behaviour of the oil companies. The differential encouraged oil companies to develop and use a no-lead lubricating additive that could be used in older cars. The older cars were previously in need for lead to provide the lubricating effect for the valves. Further, it provided oil companies with an incentive to participate in information campaigns in order to increase the market share of unleaded petrol.

As the taxes are imposed on vehicle drivers only, they can be said to have some income-distributional concerns incorporated, particularly in light of the fact that public transport is exempted from the taxes. This assumes, of course, that it is mainly the lower-income groups who do not have a car at their disposal. In that sense, the system (including also the vehicle tax system) indirectly provides for an income redistribution between wealthier (vehicle possessing) groups of society to less wealthy groups that do not possess a car. In this regard, it should also be noted that the Danish tax system allows some tax deductions to cover part of the work-related transport. This is independent of whether private or public modes of transport are used.

5.4. Tax on tap water

Well-supplied with groundwater

Denmark is well supplied with groundwater of a drinkable quality. The almost immediate use of groundwater (with very little treatment) as tap water is an area of specific priority in Denmark. The current tap water use constitutes about 2/3 of the available annual water resource. Consumption has been stagnant since the 1970s. Since 1991 the consumption has even decreased as illustrated in Table 5.4.

Table 5.4

Supply of Tap water in Denmark. Million m3/year.

1991 |

1992 |

1993 |

1994 |

1995 |

551,2 |

539,6 |

512,5 |

493,2 |

480,8 |

* excl. water recovery for large industry, the agricultural sector and fish farming when this is based on single wells. Denmark’s Statistic in 10 years, 1997

Consequently, the present level of tap water consumption does not pose a threat to the groundwater resources. Still, there are regional differences in Denmark. In some parts of the country the groundwater level is fairly low during summer.

The 1994 tax reform aimed to attach an economic value to the use of natural resources and environment in order to minimise over-consumption and the strain on the environment. Within the frames of the 1994 tax reform, a new charge on tap water was introduced and has been in effect since 1994.

5.4.1. Purpose

Consumers shall pay for a natural good

The purpose of the tap water tax is to make consumers pay for the use of a natural resource, thereby, consumers have an incentive to avoid unnecessary tap water use. The tax has another important effect, because used tap water is mostly discharged as sewage. Thus, the underlying purpose is to decrease the amount of sewage discharged to the sewage plants. This will lead to a decline in the discharges of pollutants into watercourses, lakes and seas. The treatment plants typically treat the sewage down to a pre-fixed concentration level of pollutants.

Further, the tax was also intended to provide an incentive to water companies to maintain their water pipes in a state that would minimise the leakage of water during distribution. This is further explained below.

For competitive reasons, the tax applies to neither industry, nor agriculture.

5.4.2. Tax base

The households pay the tax

The tax is levied on the water companies. The companies in turn collect the payments from the households. The exemption of industry and agriculture is effectuated through the VAT system. All VAT-registered enterprises and firms pay the tax, but they receive a full tap water tax refund upon payment of their VAT. The service sector is not entitled to a similar refund.

The tax was introduced gradually following the scheme shown below. By 1998, the tax was fully implemented at its final level of 5 DKK/m3. This corresponds to around 15-20% of the average price on water (including sewage fees and taxes).

Table 5.5

Introduction of tap water tax in Denmark.

Year |

1994 |

1995 |

1996 |

1997 |

1998 |

Tax rate. DKK/m3 |

1 |

2 |

3 |

4 |

5 |

The tax is also levied on private properties whose tap water comes from a private well instead of a public or private water company. In these cases the dutiable water consumption is calculated on the assumption that the amount of tap water use is 170 m3 annually for each household.

The water companies

The second purpose of the water tax is to minimise leakage of water as a consequence of a poor maintenance of the water pipes. This purpose is also incorporated into the tax base. The water companies must always pay tax for at least 90% of the abstracted water, no matter whether they actually end up having provided the consumers with less (due to leakage) than the 90%. The 90% figure is motivated from the fact there will always be some leakage no matter the level of maintenance. Consequently, if, for example, only 80% of the abstracted water is actually delivered to the end-users, the water company will actually be liable to a higher tax payment (for 90% of the abstracted water) than the amount they can reclaim from consumers (tax payments for the 80% only).

5.4.3. Collection and revenue

The tax is clearly shown on the water bill

The public and private water companies must register with and pay the tax to the Department of Customs and Excise. The tax is fully passed on to consumers, because they pay the tax through their water bills. The tax is explicitly written on the bill to the households in order to make it clearly identifiable. Thus, the basic principle is that the water companies collect the tax from the households and forward it to the Department of Customs and Excise.

In Denmark, the estimation of the liable tax is based on the actual consumption of tap water. From January 1, 1999, all private houses are required to have water meters installed. However, there are exceptions from the liability to install meters. For example, apartments do not have to do this, although meters may of course be installed. In this case, meters are, however, typically installed for the whole block and the payments distributed among the households according to agreed principles.

Before January 1,1999, it was not mandatory to install meters. In cases where meters were not installed, the tax was calculated based on an estimate of 170 m3 being consumed, rather than the actual use of tap water. The estimate of 170 m3 was deliberately set at a fairly high level in order to provide an incentive for consumers to install water meters. A clear trend could actually be observed of water meters being installed on an increasing scale and on a voluntary basis up until the introduction of the mandatory requirement to do so. In buildings such as summer cottages that are not used all the year, and where meters are not installed, the tax base is estimated at a consumption level of 70 m3 per year.

Table 5.6

Revenue from the tap water tax. 1995-1998.

Year |

1994 |

1995 |

1996 |

1997 |

1998 |

Revenue. MDKK |

295 *) |

654 |

970 |

1279 |

1,544 |

*) this is based on a collection of revenues for 11 months of the year – the registration of payments is one month behind.

Source: “Finanslov for finansĺret 1999” and ”Statsregnskab for finansĺret 1998”

5.4.4. Assessment

Table 5.4 shows a clear trend of a declining water supply in Denmark. In the period of 1991-1995, it declined by 13%. There are four major reasons for this decline:

| awareness building such as information campaigns; | |

| the increased water user fees during the period; | |

| the increased use of water meters; and | |

| the introduction of the tax in 1994. |

The information on revenue during the period of 1994-1998 (Table 5.6) may be used to provide an estimate of the development in water consumption in this period. The result of this is shown in Table 5.7.

It should be emphasised that figures taken from Table 5.4 and estimates based on Table 5.6 need not be comparable[10]. Nevertheless Table 5.7 indicates that reductions in water use were mainly achieved in the period prior to the introduction of the tax on tap water.

The combination of increased water prices with the option of either paying a fixed rate corresponding to 170 m3 per year or payments according to meters, have encouraged households to install meters. This has, in turn, provided an incentive for water savings, because such savings are fully reflected in reduced payments.

If industry was liable to the tax to the same extent as households, this could significantly increase the water saving potential, but it would in turn impact negatively on industry’s competitiveness.

Table 5.7

Estimated amounts of tap water liable to the tap water tax. 1994-1997.

Year |

1991 |

1992 |

1993 |

1994 |

1995 |

1996 |

1997 |

Water supply. m3 (Table 5.4) |

551 |

540 |

513 |

493 |

481 |

||

Liable amounts of water. m3 |

295 *) |

327 |

323 |

320 |

*) this is based on revenue information that covers 11 months of the year.

Source: Statistics Denmark. Statistisk tiĺrsoversigt. Tema om Miljř. 1997

The rationale for the tax is motivated from the wish to tax the use of a natural resource. Ideally, the tax should reflect the scarcity of this resource. This would, however, imply that the tax would be high in some areas and low (or even nil) in others. For efficiency and income-distributional reasons, this has not been considered desirable.

While the strict environmental motivation (the taxing of the use of a scarce resource) for the tax is fairly weak under the current conditions, where ground water resources are fairly abundant at present, the tax still has a number of environmental merits, that is:

| it enhances consumers’ awareness of the issue and thereby it contributes to enhancing the general environmental awareness of the public; | |

| it contributes to reduce the sewage amounts. All discharge water is subject to similar treatments[11]. Treatment plants typically treat the sewage to a specific individually determined concentration of P, N, and O. Reduced tap water use will inevitably lead to reduced amounts of sewage. The sewage would still be treated down to the given concentrations of P, N, and O, however, as the amount of sewage is reduced, so also is the amount of pollutants (N, P and O) that are discharged to the aquatic environment from sewage plants, and | |

| it can be seen as a preventive measure that contributes to prevent increased tap water use. |

In regard to its effect on the level of maintenance and repair of pipe systems, it is difficult to assess whether it has had any effect. The design of the tax, however, would indicate that for pipe systems in a relatively poor shape, savings achieved from reduced leakage could be sufficient to cover the costs of repair.

The collection scheme applied is based on the already existing systems for the collection of water related user fees, thereby reducing the additional administrative burden for the water companies. Furthermore, the water companies administer and collect the tax from all users in a similar way, and are not concerned with or involved in the tax refund. This is bilaterally dealt with by the Customs and Tax Department and the individual entity in question, and is effectuated through the VAT collection. Consequently, no new mechanisms were introduced, as the tax has been implemented solely through the use of existing systems.

5.5. Tax on certain retail containers

In June 1998, the Danish Parliament agreed to expand and revise the existing tax on containers that only applied to bottles and jars into a broader “tax on certain retail containers”:

Until June 1998 the tax was based on the volume of the container and applied only to bottles and jars. Since January 1, 1999, the tax has instead been based on the weight of the materials used for a wider range of containers.

- The new tax implies an extension of the scope of the tax to cover more types of commodity groups than before.

The Danish Folketing adopted the new tax in 1998, and it entered into force on January 1, 1999.

The former volume-based tax covered bottles and jars that were used as containers of liquid substances. The liquid substances covered by the tax were alcoholic liquors, wine, beer, soft drinks, water and mineral water, juice, vinegar oil, sweet oil, and methylated spirits.

In some cases, the new tax is still volume-based. Thus, for retail containers used for beer, wine, and carbonated soft drinks, the tax remains volume-based. The reason is, that in these cases, the tax is strongly related to the returnable bottle system that has been in place in Denmark for many years. This system is further described in chapter 8.

For all other applications, the tax is a weight-based tax.

The weight-based tax applies to a number of container materials. These are summarised in Table 5.8.

Table 5.8

The tax base for the tax on certain retail containers

Tax type |

Packaging type |

Applications covered |

Volume based tax |

bottles with a volume < 20 litre |

liqueur; |

Weight based tax |

paper; |

mineral water, lemonade and other drinks that

are non carbonised; |

An individual tax rate applies to each of the different materials, but similar tax rates are used for all applications. Thus, the weight-based tax level is determined only by the container material used for the container in question. Only a certain pre-defined number of applications are, however, covered by the tax.

The new weight-based tax is similar to the German user charge on certain retail containers. Germany is a major trade partner for Danish industry. It is assumed that this fact can contribute to the ease of the administrative burden on Danish enterprises that trade with partners in Germany.

5.5.1. Purpose

The tax aims to reduce the amounts of packaging material used and disposed of, thereby contributing to the reduction of the use of resources used to produce packaging material, and more importantly, the amounts of packaging waste to be disposed of.

The applications covered by the tax are shown in Table 5.8. The number is fairly limited at present, but it is expected that a wider range of applications will become liable to the tax in the future. It is the initial intention, however, to introduce the system on a more limited scale, and to carefully monitor the results achieved, and the problems encountered in the first years of the tax. Experience will thereby be gathered on the effects of the tax. This experience will be used to improve the environmental and technical knowledge on feasible options to reduce the use of packaging material.

5.5.2. Tax base

The tax on certain retail containers consists of two types; the volume based tax and the weight based tax. The tax base is illustrated in Table 5.8. The tax rates are shown in Table 5.9 for the weight-based tax.

Table 5.9

Weight-based tax rates for certain retail containers

Packaging material |

Rate, DKK/kg. |

Flexible fibre based material |

19,50 |

Fibre based materials |

7,50 |

Recycled, non-flexible, fibre based material |

6,00 |

Glass and Ceramics |

0,75 |

Plastic: |

|

Laminate |

15,00 |

Aluminium |

11,25 |

Tinplate and other steel containers: |

|

Wood |

6,00 |

The tax rates for the volume-based rate are shown in Table 5.10.

Table 5.10

The volume-based tax rate for certain retail containers

Volume |

DKK per container |

|

Containers of cardboard/laminates |

Containers of other |

|

Volume < 10 cl. |

0.15 |

0.25 |

10 cl. < Volume > 40 cl. |

0.30 |

0.50 |

40 cl. < Volume > 60 cl. |

0.50 |

0.80 |

60 cl. < Volume > 110 cl. |

1.00 |

1.60 |

110 cl. < Volume > 160 cl. |

1.50 |

2.40 |

160 < Volume |

2.00 |

3.20 |

Source: Ministry of Taxation, 1999

5.5.3. Collection and revenue

All enterprises liable to the tax must register with the Department of Customs and Excise. Liable enterprises are:

| enterprises that bottle, fill up or pack goods within the above-mentioned commodity groups (applications); | |

| enterprises that import goods that were packed abroad (including also other EU countries); and | |

| firms that act as intermediaries and/or firms that trade in unused packaging materials. |

Compared to the old tax, the new tax will lead to a substantial increase in the number of liable enterprises.

The tax applies only to materials that are used for containers. It does not apply to the similar materials when they are used in the production of goods. The liable enterprises must, therefore keep separate accounts on the amounts of materials used to produce retail containers.

Liable enterprises must notify the tax authorities. The Department for Customs and Excise will issue a registration certificate to the enterprises.

The tax authorities undertake the control of the enterprises. Enterprises must keep their accounts, so that the tax authorities can effectuate the control. Employees in the businesses are obliged to assist the tax authorities with any information they may require on the accounts submitted to the authorities.

Non-compliance, including non-payment of taxes, is sanctioned with fines.

In 1998, the revenue from taxes on retail container amounted MDKK 809. The expected revenue from the tax in 1999 is MDKK 950.

5.5.4. Assessment

The previous, more narrowly defined volume-based tax, did not provide a sufficient incentive for producers to reduce the amounts of materials used for packaging. To illustrate this, one litre of mineral water can be contained in either a bottle with a thick layer of plastic, or a bottle with a thin layer of plastic, and the tax did not differentiate between these two options.

The weight-based tax thus provides an incentive to use less material, although it should be noted that certain applications are still subject to a volume-based tax.

In regard to the weight-based tax, the efficiency of the tax structure (i.e. the set of rates shown in Table 5.9) is an important issue. In this regard, efficiency concerns may, among other things, relate to:

| the extent to which the tax level is sufficient to provide a significant economic incentive to an actual reduction in the use of the packaging materials; | |

| the extent to which the tax encourages the use of materials which are less environmentally harmful at the expense of those that are more environmentally harmful. It should be noted that the tax does not aim to pursue this objective. Rather, the tax aims to reduce the use of container (packaging) material within each group of packaging types covered by the tax; | |

| the extent to which the tax structure reflects the actual substitution and reduction possibilities. Ideally, each tax rate should be set to provide a sufficient incentive for behavioural changes which are economically feasible, and have a positive net environmental impact; | |

| the extent to which the system is comprehensive, in the sense that it does not encourage any undesired behavioural effects. This could, for example, be that the tax, in some cases, encouraged more use of materials that are more environmentally harmful, but not covered by the tax. | |

| the extent to which the tax has negative effects on the competitiveness of Danish industry; | |

| the extent to which the tax imposes too large administrative burdens on industry, compared with the environmental benefits achieved. |

It is, however, too early to assess the efficiency of the tax. It has only been in force for about two years. However, it remains a fact that the new tax is more directly targeted at environmental objectives, and it is also more ambitiously designed in that regard. In the longer run, it is expected that the weight-based tax will be replaced by an even more environmental-based tax. This could, for example, be based on life cycle assessments.

5.6. Tax on disposable tableware

The tax on disposable tableware has been in effect since 1982. It applies to tableware made of plastic materials and to the chemicals contained in the products (the disposable tableware). A minor change to the tax was prepared in 1998, and entered into force on Apri1 l, 1998. The change was motivated by a need for administrative simplifications. Previously, the tax applied to disposable plastic tableware as such, and to disposable tableware that contained some chemicals substances. The revised tax defines both the product (disposable tableware) and the chemical substances in it as disposable tableware.

5.6.1. Purpose

The tax on disposable tableware aims to reduce waste volumes and to promote recycling. Hence, its motivation is highly environmental, although it also has a fiscal purpose.

5.6.2. Tax base

The tax is imposed on the producers of disposable tableware and on those who either trade in or import these goods. The tax is also value-based. Initially, the tax level corresponded to 1/6 of the dutiable value. Since 1989, however, the tax has been set at a rate of 1/3 of the wholesale price of the product (this corresponds to 50% of the price exclusive of VAT). For imported tableware, the tax rate is 50% of the import value.

5.6.3. Collection and revenue

The producers and importers must register with the Department of Customs and Excise. The tax authorities can allow a specific business not to register if its annual dutiable turnover is less than the DKK 10,000, or if it is less than 1/3 of the turnover of the dutiable goods.

The registered businesses are to pay the tax on dutiable tableware, unless the tax duty is transferred to another registered business. However, there are certain exemptions from the liability to pay the tax; for instance, in cases where goods have been damaged and cases of fire or burglary.

The businesses must report on amounts of disposable tableware by the end of each month. If the tax is below DKK 50 the business does not have to pay each month, but can add the taxes up until they amount to more than DKK 50.

Revenues from the tax are small, with a declining tendency, as seen from Table 5.11.

Table 5.11

Revenue from the tax on disposable tableware. 1995-1998

Year |

1995 |

1996 |

1997 |

1998 |

Revenue, MDKK |

72 |

59 |

56 |

56 |

Source: “Finanslovsforslag 1999” and ”Statsregnskab for finansĺret 1998”

5.6.4. Assessment

The purpose of the tax is to reduce the use of disposable tableware. Table 5.11 shows that the revenue is declining. This indicates a decline in the use of disposable tableware, which may be, however, attributable to other factors, such as changes in consumer’s preferences. Still, the tax may also have had an effect.

5.7. CFC and halons tax[12]

The Danish government launched an Action Plan to reduce the use of ozone-depleting substances (ODS) in October 1988. This was a follow-up to the so-called Montreal Protocol. The Protocol sets the global framework for the phaseout of ODS. The plan contained six elements:

| efforts at the international level; | |

| a reduction plan for the use of CFC, including bans; | |

| a tax on the use of CFC and halons; | |

| legislation (use bans); | |

| a Research & Development programme; and | |

| data collection in support of control and monitoring. |

The CFC and halons tax entered into force in January 1989, and the tax level has remained unchanged since then. The use bans were implemented by a 1990 order, and were revised and tightened several times: in 1992, 1993, 1994, and 1995. Use of CFCs has been prohibited since January 1995, however, in a very limited number of cases, it is still possible to obtain a specific permission to use CFCs.

5.7.1. Purpose

The CFC and halons tax aims to provide an incentive to reduce the use of CFCs and halons. At the time when the tax was introduced, funds were also allocated for a research programme on CFC and halon. There was no earmarking though. Funds for the Research and Development programme were allocated independently from the general state budget.

5.7.2. Tax base

The tax is DKK 30/kg CFC and halon. It applies to:

| import and production of 5 CFC types and 3 halon types[13] when these were used either in the production of or in the maintenance of the following product groups: | |

| district heating pipe work; domestic refrigerators; domestic freezers; chilling and frost counters/cabinets; industrial refrigeration and freezers installations; mobile refrigeration and freezers (transportation); panels for cooling and freezing compartments; insulated doors and gates; extruded polystyrene insulation; structure foam (exempted December 1989, due to monitoring difficulties); sealing foam; mould release agents, aerosols, foghorns; and fire-fighting equipment containing halons. | |

| In 1989, flexible foam and cleaning solvents were exempted from the tax; motivated by concerns over competitiveness. The final products produced under these applications do not contain CFC. Consequently, it was not possible to tax the imported products, whereas the tax was imposed on domestic producers that used cleaning solvents and flexible foam in their production. | |

| import of products that contain the dutiable substances (as listed in footnote 13). |

To prevent negative effects on the competitiveness of Danish industry, exported products were entitled to a 100% refund. The refund was established, based on the content of CFC and halons in the exported products.

There are substantial variations in the ozone-depleting potentials of the taxed CFCs and halons. It varies from a factor 0.6 (CFC-115) to a factor 10 (Halon-1301). However, the tax is not differentiated according to the ozone-depleting potentials of each of the taxed substances. Instead, a unitary tax rate is applied.

The exemption, in 1989, of structure foam, flexible foam, and cleaning solvents from the tax, actually implied that about 30% of the CFC consumption became exempted from the tax. Moreover, these applications represented areas where substitution costs were lower than the tax. The behavioural effect of the tax since 1989 can therefore be expected to be limited.

5.7.3. Collection and revenue

There were two different collection schemes. One scheme applied to the use of CFCs and halons as such, and another applied to products that contained these substances:

Import and production of CFCs and Halons: The importers/producers must register with the Customs and Excise Department of the Danish Ministry of Taxation. They must maintain records on the flow of the dutiable substances, and on a quarterly basis pay the corresponding tax to the customs authorities.

Import and export of products containing CFCs and halons: Companies that engage in the import and export of products that contain CFCs and halons are not obliged to register. Instead, they are liable to the tax at the time of importation or exportation. Hence, taxes are dealt with through customs declarations.

It was expected that the tax would generate revenues in the order of DKK 111 million the first year, and that this would decline gradually to zero because of the use bans. However, the revenue turned out to be negative for the first year. In the following two years, it only amounted to DKK 26 million and DKK 12 million respectively.

The reasons for these low revenues were mainly:

| hoarding prior to the implementation of the tax; | |

| a faster reduction in the use of CFCs than expected; and | |

| biases in the tax collection system.[14] |

For 1998, the tax generated a tiny revenue of DKK 0.2 million. This reflects today’s small use of CFCs. The “ordinary” use of CFCs has been prohibited since 1995. Today, CFC may only be used on the condition that specific permissions have been obtained. Such permissions are granted in very few cases only, such as for analytical use.

5.7.4. Assessment

The ozone-depleting substances were phased out faster than originally anticipated. Consequently, the complete ban could be implemented earlier than expected. Already in 1995, the use of ozone-depleting substances in Denmark dropped to virtually zero. Hence, the overall CFC Action Plan was effective in achieving a rapid phaseout of ODS.

The rapid reduction in the use of CFCs and halons is, however, mainly attributable to the pre-announcement and specific timing of the use bans. This encouraged producers to accelerate the development of financially and technically feasible alternatives. This effect was further supported through the research and development programme.

Initially, it was assumed that the tax would have a significant negative effect on the use of those CFCs that had relatively low substitution costs. However, the exemption in 1989 of cleaning solvents and flexible foam from the tax implied that exactly these applications were not liable to the tax.

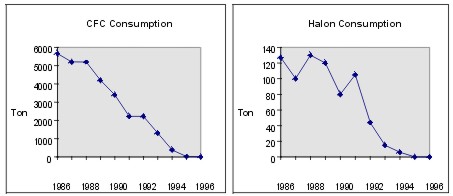

Figure 5.1

Developments in Denmark in the use of CFCs and halons. 1986-1996

Note: The zig-zag development of halon consumption is due to hoarding following the announcement of users ban on various halons.

Still, while the administrative means and the R&D programme thus had the largest effect on the use of ODS, the tax has still played a role, especially through its “signal-effect”.

5.8. Chlorinated solvents

Chlorinated solvents are substances that for many years have been considered harmful to both the natural environment and occupational health. Some chlorinated solvents deplete the ozone layer, while others possess a risk for the quality of the ground water. They are harmful for the human nerve system and some of the solvents are perceived to be carcinogenic.

The tax on chlorinated solvents is one of the relatively new and truly “green” taxes. It went into force on January 1, 1996. The tax dates back to a comprehensive report from the Ministry of Finance (1994) on green taxes[15], which outlined the options for a wider use of green taxes in general. It concluded that the existing regulation of chlorinated solvents was insufficient, and recommended a tax on chlorinated solvents as a cost-efficient means to reduce the use.

5.8.1. Purpose

The purpose of the tax is environmental. The tax aims to reduce the use of chlorinated solvents, and to provide a further incentive to develop less environmentally harmful alternatives to chlorinated solvents. Furthermore, the tax is motivated by the need to prevent an occurrence that may come from the ban on the use of the ozone-depleting CFCs (see section 5.7). That is, the need to prevent the increase in the use of chlorinated solvents (that, in some cases, can be substitutes for the CFC’s).

The tax applies to the three most commonly used chlorinated solvents. At the time of implementation, it was estimated that the use of these chlorinated solvents together accounted for 95% of the total domestic use of chlorinated solvents.

5.8.2. Tax base

The tax amounts to 2 DKK/kg of chlorinated solvent, which corresponds to a consumer price increase of about 25%. The tax applies to:

| the use of three substances: tetrachloroethylene, trichloroethylene, and dichloromethane. The current use of these substances is about 2000 ton/year; and | |

| imports of products which contain the above dutiable substances (like glue, paint and detergents). The imported amount of chlorinated solvents in these products is estimated at around 1000 ton/year. |

The tax applies to the chlorinated solvents in their pure form. It also applies, in cases where the chlorinated solvents are found in other goods if their concentration exceeds 1 percent by weight. In this case, the tax is termed a contribution tax.

There is a direct positive relation between the use of solvents (measured in kilo), and emissions to the environment. All three substances have similar environmental impacts. Consequently, the tax is well designed from an environmental perspective.

The tax on substances and products sold for export is refunded. This is motivated by concerns over competitiveness.

5.8.3. Collection and revenue

Producers and importers of chlorinated solvents, plus importers of products that contain the solvents, pay the tax to the regional offices of the Department of Customs and Excise.

Enterprises that produce (or regain and sell) the three dutiable solvents must register with the customs authorities. Registered enterprises are liable to the tax once the solvents in question leave the enterprise.

Imports of products that contain dutiable substances must be accompanied by a declaration from the manufacturer on the amount of dutiable substance in the products. Enterprises that import such products must:

| either register with the customs authorities and pay the tax when the products leave the enterprise; or | |

| report continuously to the customs authorities on products imported and pay simultaneously with this reporting. |

In 1998, the revenue from the tax on chlorinated solvents was 2.3 MDKK[16].

Table 5.12

Annual revenue from the tax on chlorinated solvents, MDKK

1996 1) |

1997 |

1998 |

3.23 |

3.26 |

2.3 |

1) the revenue comprise the 11 months of domestic use and sales of chlorinated solvents, together with the taxes paid for chlorinated solvents on stock. 2) the first figure (1.64) applies to the first eight months of the year.

The revenue of 3.26 MDKK in 1997 corresponds to a total annual use of about 1,600 tons. When the tax went into force on January 1, 1996, it was estimated that the annual use of the solvents amounted to 2,000 tons of the chlorinated solvents in their pure form, and another 1,000 tons as components of other goods. While these estimates are somewhat uncertain, the figures nevertheless indicate that already in 1997, a reduction in the use of chlorinated solvents had been achieved. Further, the table shows that from 1997 to 1998, the revenue declined by another 30%.

5.8.4. Assessment

The tax on chlorinated solvents was implemented, although there was substantial uncertainty about its exact implications. In the comments to the draft law, it is explicitly mentioned that the tax was designed without full information on, for example, options for substitution. Therefore, the comments also state that the implementation of the tax should be monitored carefully in order to identify areas where revisions or adjustments might be necessary. The tax was expected to lead to a reduction in the use of chlorinated solvents in the order of 15%.

Table 5.13 shows the development in the net-imports of the chlorinated solvents covered by the tax. The table clearly confirms the indication of significant reductions in the use of the solvents, as also indicated in Table 5.12. In regard to the table, it should be noted that analyses indicate that trichlorethylene and tetrachlorethylene are mainly used in their pure form (95% and 97% respectively of the total use), whereas, only 74% of the use of dichlormethane is in its pure form.

Table 5.13

Net-import (tons/year) of the chlorinated solvents covered by the tax 1).

Type of chlorinated solvent |

1992-1995 |

1996 |

1997 |

1998 |

Diclormethane |

483 |

278 |

||

Trichlorethylene |

1000 |

792 |

477 |

356 |

Tetrachlorethylene |

720 |

760 |

459 |

463 |

Source: Evaluering af Grřnne Afgifter for Erhvervene.

1) The table does not include imports and exports of goods containing the chlorinated

solvents. Figures for 1992/1995 and for 1996-1998 are not fully comparable as data derives

from different sources.

While the use of dichlormethane in its pure form has declined, the solvent is used in significant amounts as a component in lacquer removers.

All in all, Table 5.13 provides very strong indications that the tax has had a substantial effect in terms of having reduced the use of chlorinated solvents. The reduction appears less apparent, but is still significant, in the case of tetrachlorethylene. This could indicate that substitution barriers are stronger in the case of tetrachlorethylene.

5.9. Pesticides[17]

Pesticides are used to kill weed, pest, and pathogenic fungi, thereby improving agricultural yield. However, pesticides spread into the environment and may cause pollution of soil, water, and air. During recent years, increasing amounts of remnants of pesticides have been detected in crops, watercourses, lakes, groundwater, and soil.

Denmark has had a national pesticide plan since 1986. Its purpose is to protect the pesticide users, the general public, and the environment from the hazards of pesticides. The plan aims to halve pesticide use by 1997, compared with the use in 1981-1985.

The use of pesticides is measured as:

| the amount of active ingredients used (measured in kg); and | |

| the number of doses applied per hectare of cultivated land (called treatment intensity). |

A number of initiatives have been taken to pursue the objectives of the plan: stricter environmental standards for the use of pesticides; mandatory education schemes for all farmers who use pesticides; and mandatory supervision of pesticide application equipment. Agriculture counts for approximately 90% of the pesticide consumption in Denmark. Farmers are also obligated to keep records of the quantity and types of pesticides used on each field.

The tax on pesticides was implemented on January 1, 1996 as a further means to promote the targeted reduction in pesticide use. The tax in itself aimed to reduce pesticides use by 10%. A tax increase took effect November 1, 1998. The purpose of the increase was to achieve a further 10% reduction.

5.9.1. Purpose

The purpose of the pesticide tax is to reduce the use of pesticides. Due to difficulties of measurement, the tax is not differentiated according to toxicity or other indicators of the relative health and environmental impacts of the different pesticides. Insecticides are taxed heavier than other pesticides. This merely reflects the fact that insecticides are cheap. Therefore, insecticides must be imposed with a larger tax in order for the tax to have an effect.

5.9.2. Tax base

The tax base for the most important pesticides – insecticides, herbicides, and fungicides – is the retail price of the pesticides. This is defined as the maximum retail price for every single pesticide. The fact that the tax is based on retail prices requires a strong monitoring of retail prices. This is achieved through a price label system, which indicates a maximum selling price. Pesticides may not be sold at prices that exceed the maximum price, and retailers who sells at a price lower than the maximum price, or who offer a rebate, will not be entitled to corresponding tax refunds.

Table 5.14

Pesticides tax. Tax base and tax rates.

Pesticides |

Tax base |

Tax rate |

Insecticides, etc. |

|

|

Herbicides |

retail price |

33.33% of retail price, excl. tax |

Fungicides, etc. |

|

|

Wood preservatives, etc. |

|

|

Note: Before November 1, 1998, the tax rates for insecticides and fungicides were 35% and 27% respectively, whereas the tax on wood preservatives was the same as now.

5.9.3. Collection and revenue

The tax is imposed at the level of manufacturing and import. This reduces the costs of control and administration, because the number of companies registered at this level is considerably smaller than at the retail level. Enterprises that produce or import the dutiable pesticides must register with the customs authorities.

In 1998, the revenue amounted to MDKK 298 [18]. It is expected to increase to MDKK 355 in 1999, as a result of the tax rate increases in November 1998[19].

Simultaneously with the tax, property taxes were reduced for agricultural properties. The tax and the reduced property taxes are legally and financially independent. Nevertheless, the reduced property taxes are to be considered as deficiency payments to agriculture. A similar observation applies to the recently introduced scheme to provide financial support for the development of organic farming. This scheme was introduced simultaneously with the increased pesticides tax on November 1, 1998.

5.9.4. Assessment

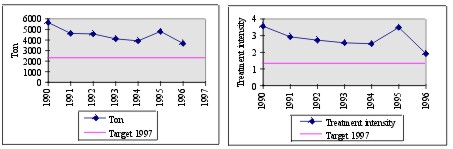

The tax was implemented on January 1,1996. Consequently, the significant increase in pesticide sales in 1995 may be due to hoarding behaviour prior to the entry into force of the tax. The perceived hoarding in 1995 may also have impacted negatively upon the estimates on the use in 1996. Therefore, it is necessary to consider these two years jointly in an assessment of the effects of the tax. The treatment frequency for 1995 and 1996 together can be assessed to be 2.71. In 1997, this figure had dropped to 2.45. Developments thus show a movement towards the ultimate target of 1.34.

Figure 5.2

The development of the pesticide use in Denmark, 1990-1996. Amount of pesticides used and

treatment intensity

The absence of a reliable and unambiguous environment-load index implies that the tax scheme does not reflect the environmental and health pressures caused by the different types of pesticides. Consequently, it could be a step forward if an environment-load-index could be established to constitute the basis for setting the tax rates. It is, however, highly uncertain whether this can practically be achieved.

The lack of an environmental load index implies that the tax has not been constructed with a particular view to the relative toxicity of the various pesticides. However, the tax has definitely lead to a decline in the overall treatment frequency, in accordance with the intention of the law.

The environmental effects of the tax are mainly achieved through its impact on overall demand and consequent treatment frequencies. It has virtually no impact on the supply side, because pesticides products are developed and sold by large international companies. Denmark is only one, fairly small, local market for these companies.

5.10. Tax on growth promoters[20]

Growth promoters are used as additives to fodder in order to increase the growth of animals. In Denmark, approximately 100 tons of growth promoters were used annually in the period 1991-1997. Approximately 80% were consumed in the production of piglets and porkers.

In recent years, a lively debate has taken place on the relation between the use of growth promoters and animal welfare. It is argued that the use of growth promoters is contradictory to the rules of conduct for sound farming.

Consequently, the tax on growth promoters went into force on September 1, 1998. The tax aims to reduce the use of growth promoters by 60-70%. Other and more far reaching initiatives, soon overshadowed the tax. These initiatives are expected to lead to an eventual total phase-out of growth promoters by January 2000. The initiatives are:

- An agreement to regulate the use of growth promoters used in raising cattle, broilers, and porkers (over 35 kg), made between the producers and slaughterhouses. The agreement was signed and took effect in spring 1998. As a consequence of the agreement, the use of growth producers was reduced by 37.5% during the first half of 1997, i.e. even before the tax went into force.

- Between 96% and 98% of all porker producers – by far the most important producer group in regard to growth promoters – have signed an agreement in which they voluntarily agree to omit the use of growth promoters. Porker producers that have not signed the agreement must pay a penalty payment to the slaughterhouse of DKK 0.20/kg meat. This level is considered high enough to provide sufficient incentive to join the agreement. Actually, the penalty payment is likely to affect the producer even more than the tax.

- Following an intense debate in the national media in September 1998, the agricultural organisations declared a total and voluntary stop for the use of growth promoters in Danish agriculture. This also includes the production of piglets. The voluntary ban would take effect from January 1, 2000. It is conditioned on the outcome of a major research programme launched in the Autumn 1998, which seeks to develop effective substitutes for growth promoters. At present, it is the expectation of the agricultural organisations that the use of growth promoters will stop in late 1999.

5.10.1. Purpose

The tax aims to reduce the use of growth producers by 60-70%, thereby contibuting to the establishment of the conditions for a sound agriculture production. Furthermore, it provides an incentive for the users to make voluntary agreements to stop the use of growth promoters.

5.10.2. Tax base

The tax on growth promoters is a product tax. It is imposed on “pure” growth promotion substances and on imported products that contain growth promoters. Table 5.15 illustrates the tax levels and the types of growth promoters covered by the tax.

Table 5.15

Tax levels for dutiable Growth Promoters

Substance |

Tax level |

Zinkbacitracin |

DKK 1 / gram |

Spiramycin |

DKK 1 / gram |

Virginiamycin |

DKK 1 / gram |

Flavofosfolipol |

DKK 2.5 / gram |

Tylosinfosfat |

DKK 1.25 / gram |

Monensin natrium |

DKK 1 / gram |

Salinomycin natrium |

DKK 0.83 / gram |

Avilamycin |

DKK 1.25 / gram |

Carbadox . |

DKK 1 / gram |

Olaquindox |

DKK 1 / gram |

EU regulations establish maximum values for the allowed amounts of growth promoters to be blended with the fodder. The maximum values differ from one growth promoter to another. The EU regulations were taken into account when setting the tax levels shown in Table 5.15, thereby, the tax levels have been set to ensure that the cost effect per pig is the same, regardless of which growth producer is used. Consequently, additives that need to be used in large quantities, and where maximum values are correspondingly high, are taxed lower than additives that need only be used in small amounts.

The tax rates shown in Table 5.15 imply that the costs of producing one porker will increase by DKK 4. This corresponds to the net economic gain from the use the growth promoters. Consequently, the tax has removed the economic incentive to use growth producers in porker production. Porker production accounts for the major share of the use of growth promoters.

However, the tax is not sufficient to fully remove the economic incentive to use growth promoters in the production of piglets. The tax increases the cost per piglet by DKK 4-5 while it is assumed that the net economic gain from the use of growth promoters lies in the range of DKK 10 per piglet.

5.10.3. Collection and revenue

The tax is levied on production and import of growth promoters and on the import of products containing growth promoters. The affected entities shall pay the tax to the Department of Customs and Excise.

Those liable to the tax are:

| producers of growth promoters. Such enterprises must register with the national customs authorities (The Department of Customs and Excise). They are obligated to keep record of the production and purchase of growth promoters; and | |

| importers of growth promoters. Such enterprises likewise must register with the national customs authorities and must keep record of the purchase and deliveries for every one of the ten dutiable growth promoters. |

Every month the registered enterprises must calculate the liable amount of growth promoters, i.e. the amount of growth promoters sold by the enterprise as well as its own use.

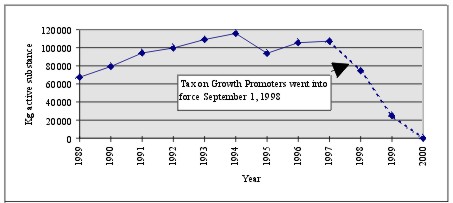

The realised revenue for 1998 was DKK 16 millions. The past and expected trends in the use of growth promoters are illustrated in Figure 5.3. The figure clearly illustrates that the used growth promoters declined already prior to the entry into force of the tax.

Figure 5.3

Actual and estimated use of growth promoters in Denmark 1989-2000

Sources: Information on consumption from 1989-1996 is based on Dansk Veterinćrtidsskrift, 1998, 81, 8. The consumption for 1997 and 1998 is based on figures from Ministry of Food, Agriculture and Fisheries. The figure for 1998 is a projection of the consumption in the first six month of 1998. Information on expected consumption in 1999 and 2000 is given by Landbrugsraadet (the main Danish agricultural organisation).

5.10.4. Assessment

The tax has been designed to completely remove the economic incentive to use growth promoters in porker production; the single most important area of use. The tax would thus be expected to lead to substantial reductions in the use of growth promoters. In the case of piglets, the economic gain from the use of growth promoters will be somewhat reduced by the tax, although there will still be an economic advantage.